Accrual Accounting

Accrual Accounting

Liabilities and Owner's Equity

Let's begin our analysis of your beginning balance sheet with the liabilities and owner's-equity sections. We're assuming that, thanks to a strong business plan, you've convinced a local bank to loan you a total of $125,000 - a short-term loan of $25,000 and a long-term loan of $100,000. Naturally, the bank charges you interest (which is the cost of borrowing money); your rate is 8 percent per year. In addition, you personally contributed $150,000 to the business (thanks to a trust fund that paid off when you turned 21).

Assets

Now let's turn to the assets section of your beginning balance sheet. What do you have to show for your $275,000 in liabilities and owner's equity? Of this amount, $50,000 is in cash - that is, money deposited in the company's checking and other bank accounts. You used another $75,000 to pay for inventory that you'll sell throughout the year. Finally, you spent $150,000 on several long-term assets, including a sign for the store, furniture, store displays, and computer equipment. You expect to use these assets for five years, at which point you'll probably replace them.

Income Statement

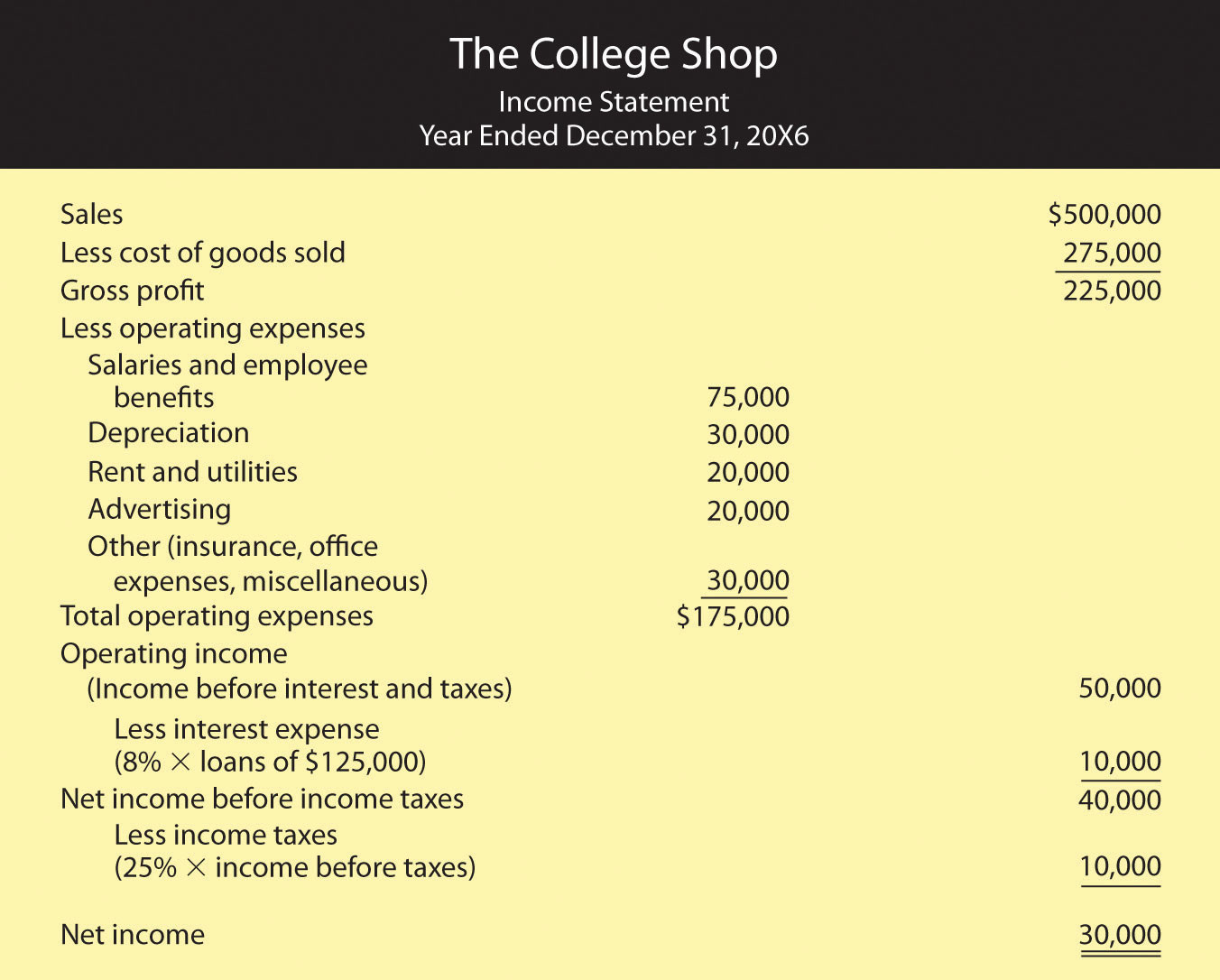

Finally, let's look at your income statement, which is shown in Figure 12.15 "Income Statement for The College Shop, Year Ended December 31". Like your College Shop balance sheet, your College Shop income statement is more complex than the one you prepared for Stress-Buster, and the amounts are much larger. In addition, the statement covers a full calendar year.

Figure 12.15 Income Statement for The College Shop, Year Ended December 31

Note, by the way, that the income statement that we prepared for The College Shop is designed for a merchandiser - a company that makes a profit by selling goods. How can you tell? Businesses that sell services (such as accounting firms or airlines) rather than merchandise don't have lines labeled cost of goods sold on their statements.

The format of this income statement also highlights the most important financial fact in running a merchandising company: you must sell goods at a profit (called gross profit) that is high enough to cover your operating costs, interest, and taxes. Your income statement, for example, shows that The College Shop generated $225,000 in gross profit through sales of goods. This amount is sufficient to cover your operating expense, interest, and taxes and still produce a net income of $30,000.

A Few Additional Expenses

Note that The College Shop income statement also lists a few expenses that the Stress-Buster didn't incur:

- Depreciation expense. Recall that before opening for business, you purchased some long-term assets (store sign, displays, furniture, and equipment) for a total amount of $150,000. In estimating that you would use these assets for five years (your estimate of their useful lives), you spread the cost of $150,000 over five years. For each of these five years, then, your income statement will show $30,000 in depreciation expense ($150,000 ÷ 5 years = $30,000).

- Interest expense. When you borrowed money from the bank, you agreed to pay interest at an annual rate of 8 percent. Your interest expense of $10,000 ($125,000 × 0.08) is a cost of financing your business and appears on your income statement after the subheading operating income.

- Income taxes. Your company has to pay income taxes at a rate of 25 percent of net income before taxes. This amount of $10,000 ($40,000 × 25%) appears on your income statement after the subheading net income before income taxes. It's subtracted from income before income taxes before you arrive at your "bottom line," or net income.