Understanding Financial Statements

The Balance Sheet

Your balance sheet reports the following information:

- Your assets: the resources from which it expects to gain some future benefit

- Your liabilities: the debts that it owes to outside individuals or organizations

- Your owner's equity: your investment in your business

Whereas your income statement tells you how much income you earned over some period of time, your balance sheet tells you what you have (and where it came from) at a specific point in time.

Most companies prepare financial statements on a twelve-month basis - that is, for a fiscal year which ends on December 31 or some other logical date, such as June 30 or September 30. Why do fiscal years vary? A company generally picks a fiscal-year end date that coincides with the end of its peak selling period; thus a crabmeat processor might end its fiscal year in October, when the crab supply has dwindled. Most companies also produce financial statements on a quarterly or monthly basis. For Stress-Buster, you'll want to prepare a monthly balance sheet.

The Accounting Equation

The balance sheet is based on the accounting equation:

assets = liabilities + owner's equity

This important equation highlights the fact that a company's assets came from somewhere: either from loans (liabilities) or from investments made by the owners (owner's equity). This means that the asset section of the balance sheet on the one hand and the liability and owner's-equity section on the other must be equal, or balance. Thus the term balance sheet.

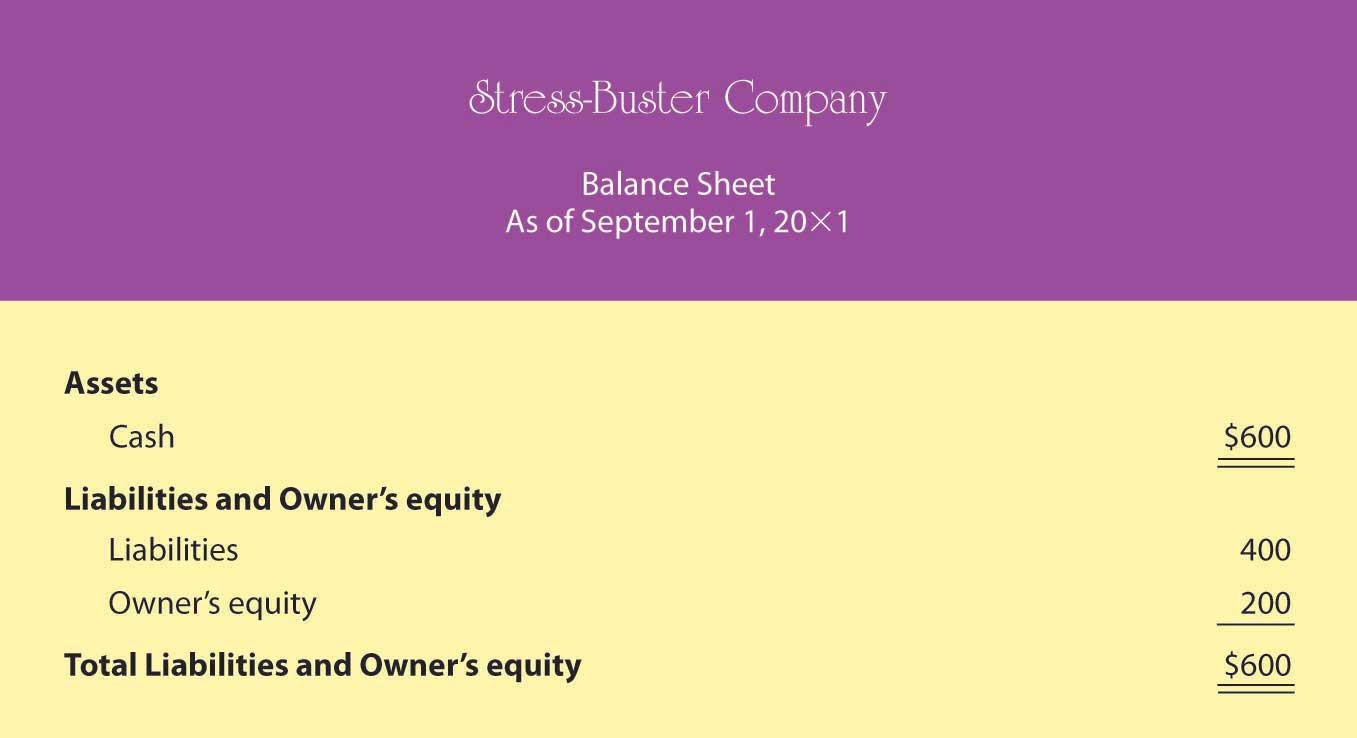

Let's prepare two balance sheets for your company: one for the first day you started and one for the end of your first month of business. We'll assume that when you started Stress-Buster, you borrowed $400 from your parents and put in $200 of your own money. If you look at your first balance sheet in Figure 12.9 "Balance Sheet Number One for Stress-Buster Company" you'll see that your business has $600 in cash (your assets): Of this total, you borrowed $400 (your liabilities) and invested $200 of your own money (your owner's equity). So far, so good: Your assets section balances with your liabilities and owner's equity section.

Figure 12.9 Balance Sheet Number One for Stress-Buster Company

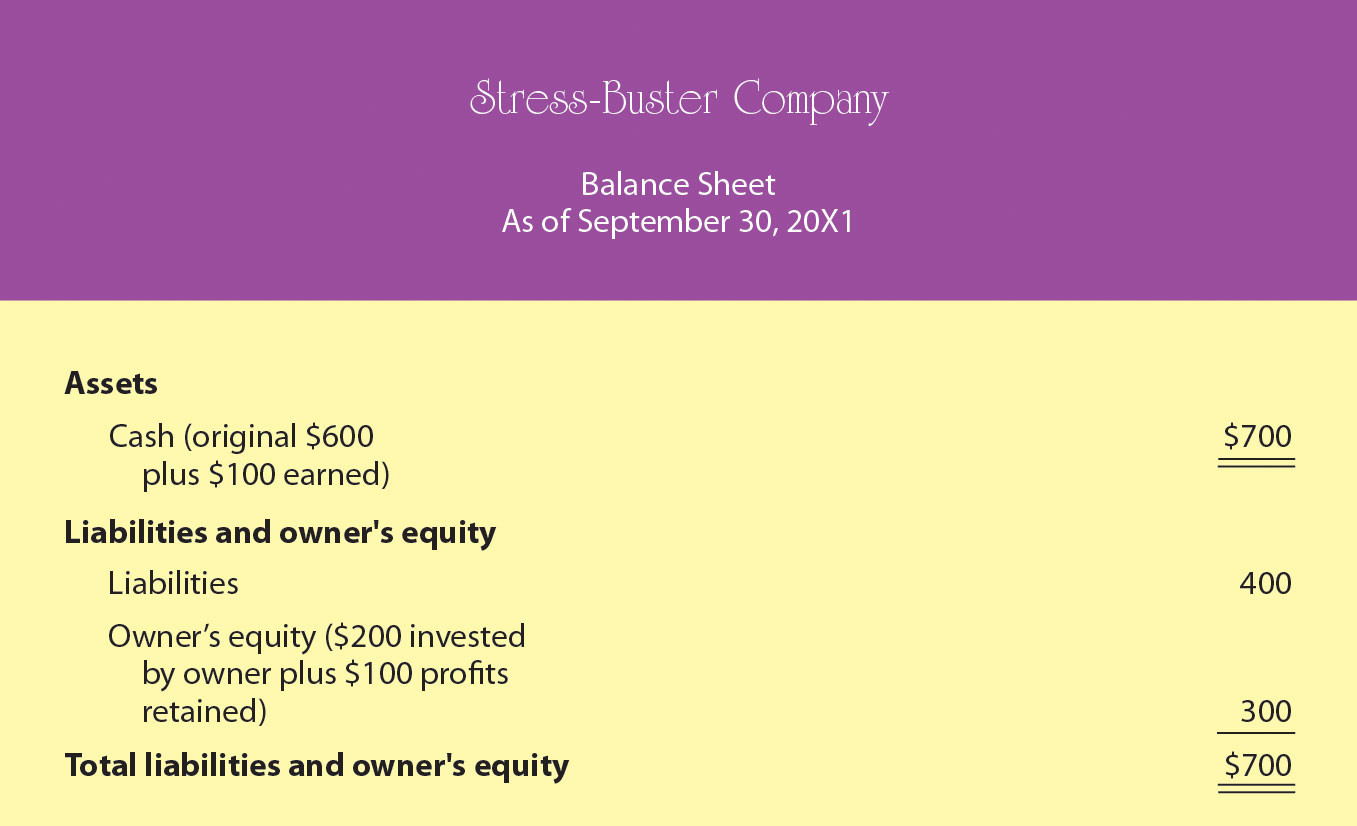

Now let's see how things have changed by the end of the month. Recall that Stress-Buster earned $100 (based on sales of 100 units) during the month of September and that you decided to leave these earnings in the business. This $100 profit increases two items on your balance sheet: the assets of the company (its cash) and your investment in it (its owner's equity). Figure 12.10 "Balance Sheet Number Two for Stress-Buster Company" shows what your balance sheet will look like on September 30. Once again, it balances. You now have $700 in cash: $400 that you borrowed plus $300 that you've invested in the business (your original $200 investment plus the $100 profit from the first month of operations, which you've kept in the business).

Figure 12.10 Balance Sheet Number Two for Stress-Buster Company