Financing Options

- 4g List and explain the tools available to the Federal Reserve during financial crises (CLO 5)

Getting the Money

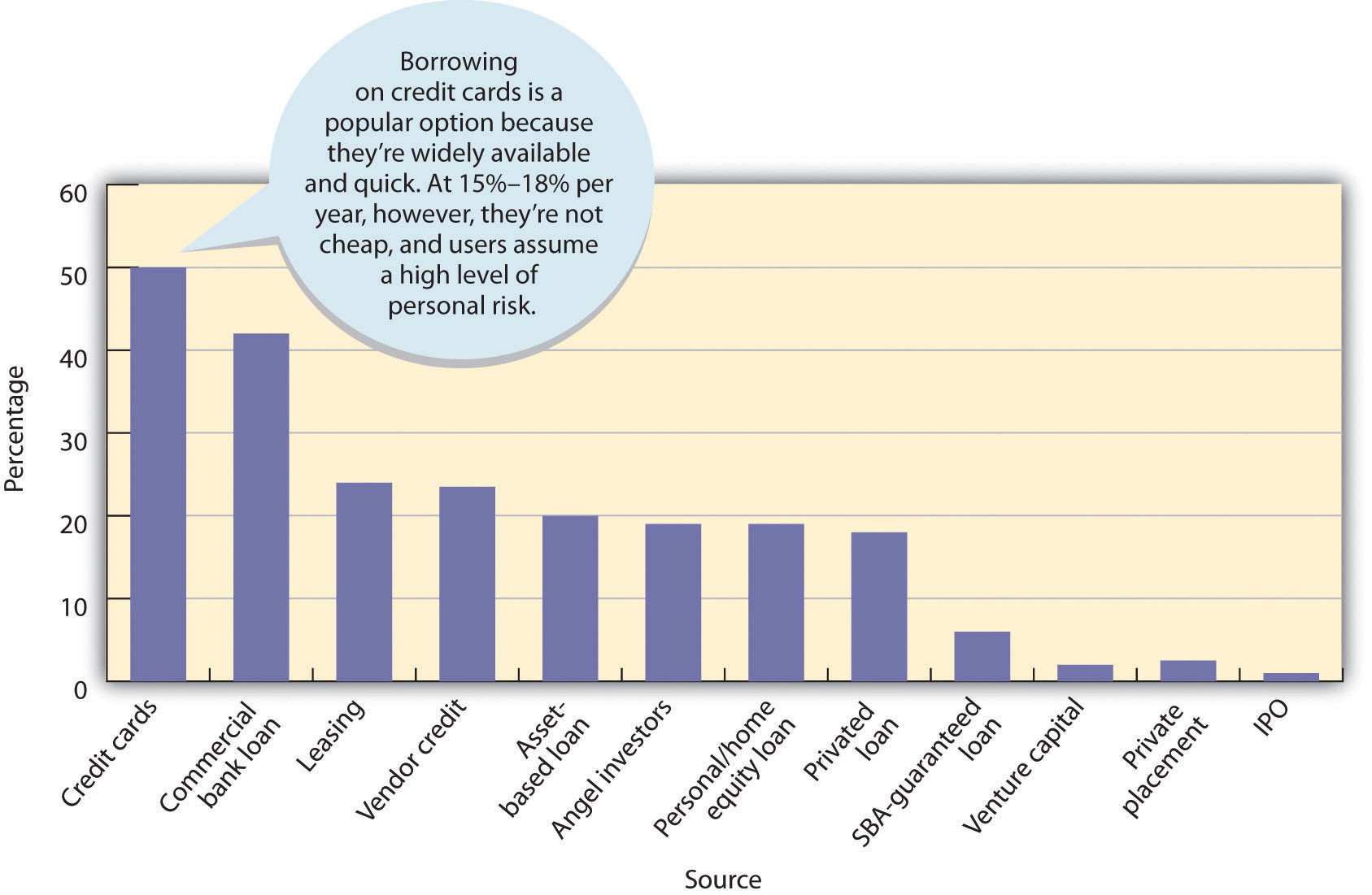

Figure 13.8 "Where Small Businesses Get Funding" summarizes the results of a survey in which owners of small and medium-size businesses were asked where they typically acquired their financing. To simplify matters, we'll work on the principle that new businesses are generally financed with some combination of the following:

- Owners' personal assets

- Loans from families and friends

- Bank loans (including those guaranteed by the Small Business Development Center)

Figure 13.8 Where Small Businesses Get Funding

Remember that during its start-up period, a business needs a lot of cash: it not only will incur substantial start-up costs, but may even suffer initial operational losses.

Personal Assets

Its owners are the most important source of funds for any new business. Figuring that owners with substantial investments will work harder to make the enterprise succeed, lenders expect owners to put up a substantial amount of the start-up money. Where does this money come from? Usually through personal savings, credit cards, home mortgages, or the sale of personal assets.

Loans from Family and Friends

For many entrepreneurs, the next stop is family and friends. If you have an idea with commercial potential, you might be able to get family members and friends either to invest in it (as part owners) or to lend you some money. Remember that family and friends are like any other creditors: they expect to be repaid, and they expect to earn interest. Even when you're borrowing from family members or friends, you should draw up a formal loan agreement stating when the loan will be repaid and specifying the interest rate.

Bank Loans

The financing package for a start-up company will probably include bank loans. Banks, however, will lend you some start-up money only if they're convinced that your idea is commercially feasible. They also prefer you to have some combination of talent and experience to run the company successfully. Bankers want to see a well-developed business plan, with detailed financial projections demonstrating your ability to repay loans. Financial institutions offer various types of loans with different payback periods. Most, however, have a few common characteristics.